The system

0.751

Sharpe

- Total return

- 15.36%

- MaxDD

- -7.77%

A multi-strategy US equities research system built around a two-layer architecture: an LLM research and critique layer (per-strategy signal specialists, an adversarial critic, and a training-time signal proposer), and a deterministic execution layer (validation, portfolio construction, capital allocation, risk controls, and OOS replay). The primary question was how to keep LLM judgment bounded while still using it where it adds value.

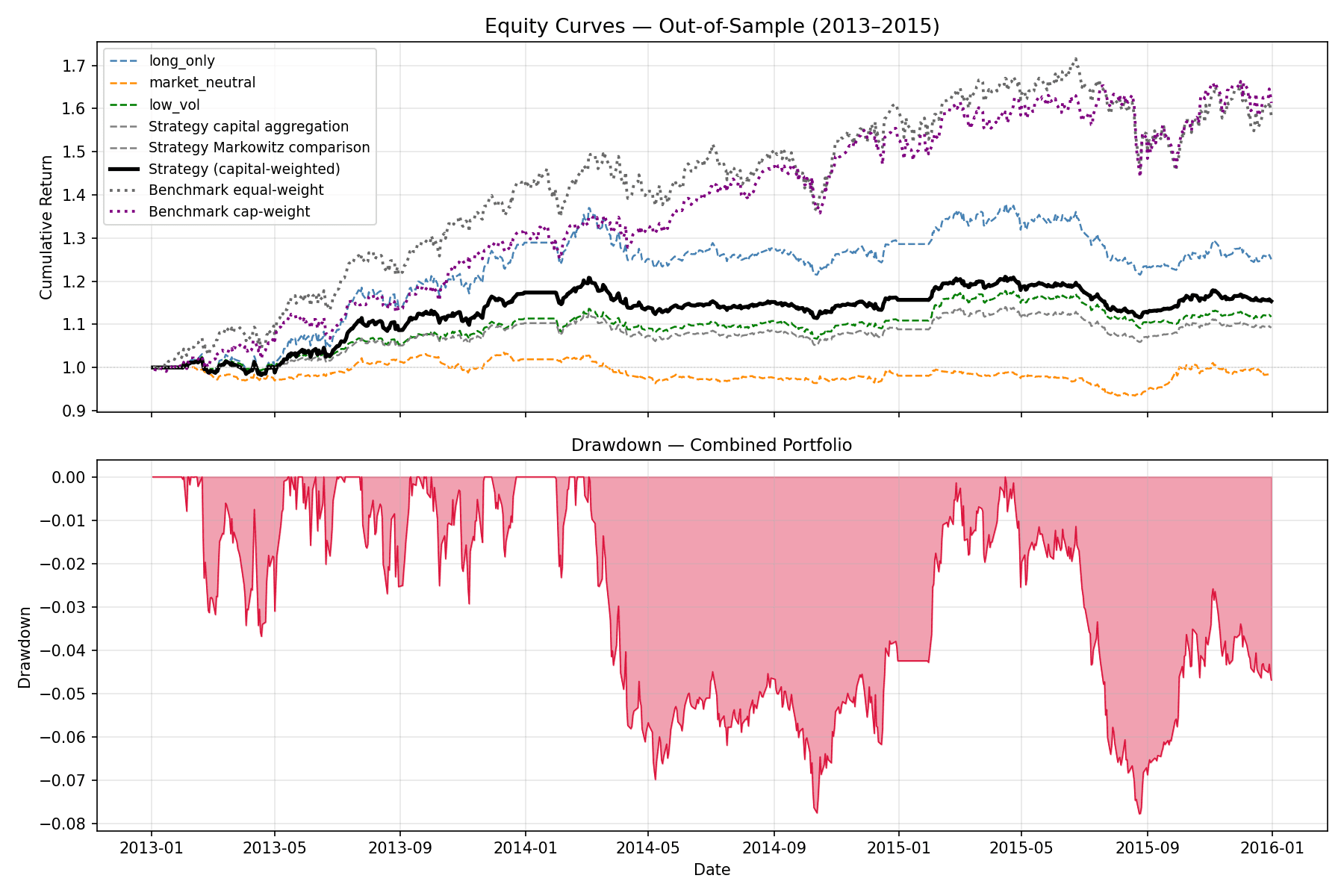

Focus: point-in-time data discipline, agentic architecture with a zero-LLM money path, pre-registered primary aggregation (capital-weighted), and honest OOS reporting — including the concentration of returns in 2013 and two near-flat years after.

Deliberately out of scope: factor-model risk decomposition (build-or-buy decision deferred), live execution reconciliation, capacity and slippage modeling beyond a flat 10bps round-trip, and multi-year OOS validation. The 2013-2015 window is spent; any further parameter changes would require a new pre-registered OOS run.

Annual walk-forward, 2013-2015

The system

0.751

Sharpe

Equal-weight universe

1.092

Sharpe

Cap-weighted universe

1.242

Sharpe

The spread is the point: over this window, broad-market beta won. The system is lower-beta and includes market-neutral exposure, so the verification result reads as beta versus alpha rather than a victory lap.

Equity curve for the system against equal-weight and cap-weighted benchmarks over the 2013-2015 out-of-sample window.

as of 2012

| PM | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | Mandate |

|---|---|---|---|---|---|---|---|---|

| long_only | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | 0.90g/0.90n |

| market_neutral | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | 1.60g/0.00n |

| low_vol | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | ACTIVE | 0.70g/0.70n / vol 6% |

All three sleeves remained ACTIVE across the training window. The structural-action layer never crossed its evidence bar, so no probation or decay action was triggered. Mandates are shown as gross/net dollar-exposure targets (with vol target where set).